Biweekly Pay Considered Harmful

Getting paid every other Friday sucks. You're not likely to notice the suckage when you're flush with cash, but when finances are tight, it really, really sucks.

I've had several conversations with friends and family who don't see why. After all, if you're making $12k a year, then who cares whether you're getting $500 twice a month, or $461.50 every other Friday? And you're getting paid sooner, which must be better, right?

Wrong. My experience with biweekly paychecks is that I constantly felt like I was falling farther and farther behind, with reprieves at the end of June and December. Nobody believed me, so I made a spreadsheet to illustrate the point.

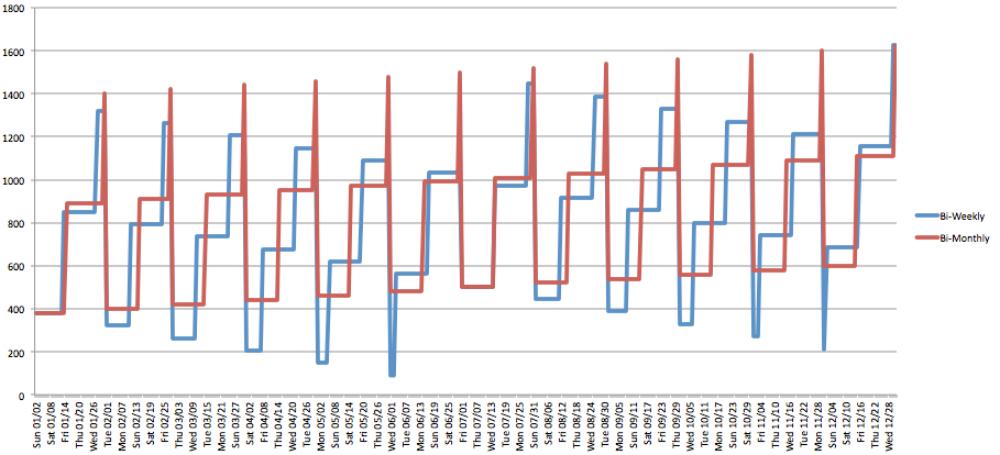

The red line is your bank balance if you're making $1020 each month, and spending $1000 on the first of each month. The blue line is your bank balance if you're making $471 every two weeks (still $1020 per month), and spending the same $1000 per month.

Lo and behold, look at the red (bi-monthly pay) line's steadily climbing peaks and valleys. Every month, like clockwork, you get a little farther ahead.

And look at that blue line, steadily dropping from January until June, when you get three paychecks and end up back on top. And at that point, you start the descent again.

And note that if you're being paid bi-weekly, whatever high points you hit are illusions-- you'd better save that cash for a rainy day, because six months from now, you're going to be behind the 8-ball once again.

This also explains two things about how I run my finances:

First, when I calculate my monthly income (when making a budget, for instance), I don't take my yearly salary and divide by 12. I take one paycheck, and double it. That's how much I can rely on to come in every month. This way, I know I can cover all my bills, regardless of whether I'm in the hights of July or January, or the depths of June or December.

This has the side-effect of forcing me to live well beneath my means. About 15% of my income is ignored when calculating my monthly budget. This is by necessity: if I lived close to my means, those downward-marching spikes on the blue line would bite into me pretty hard. As long as I have spare cash around, I don't have to worry.

Second, dropping below about $500 in my checking account stresses me out huge. Why? Because after years of being paid bi-weekly, I know I need that padding. I have to check the calendar to know when my next paycheck is coming, and figure out whether I have enough in that account to cover my bills. It's not as simple as "What's today's date?" Rather, I have to know the current date, the date that I get paid next, and the date that the bill is due. I've learned the hard way to keep that $500 "safety net" in the account, lest I end up overdrawn when a bill comes due on the first, and my paycheck arrives on the second.

I did some tinkering with the numbers. The graph above is for montly expenses of $1000 against an average monthly income of $1020. If you're getting paid bi-weekly, and want to save $20 every month, you have to reduce your expenses to about $922, nearly 8%. This means that you'll see big jumps twice a year when you get an "extra" paycheck.

Really, this is meant to illustrate the radical difference a simple scheduling difference can make. It means that in order to achieve basic goals like saving money each month, or to be able to recover from a large but unavoidable expense (car, illness, previous layoff), you have to markedly reduce your monthly expenses from what you could support if you were simply paid on the 15th and 30th.

Think about that stretch from April 15th to July 1st. You've spent your money paying your taxes, and it's only going to get worse until July.